Subscribe Email Address Sign Up Thank you! Katherine J. Reisfeld, CFP®, CIMA® 6/8/26 Katherine J. Reisfeld, CFP®, CIMA® 6/8/26 The Cost of Complexity Read More Katherine J. Reisfeld, CFP®, CIMA® 5/26/26 Katherine J. Reisfeld, CFP®, CIMA® 5/26/26 Introducing Elena Spellman Read More Katherine J. Reisfeld, CFP®, CIMA® 5/26/26 Katherine J. Reisfeld, CFP®, CIMA® 5/26/26 Is an AI Crash Coming? Read More Katherine J. Reisfeld, CFP®, CIMA® 5/19/26 Katherine J. Reisfeld, CFP®, CIMA® 5/19/26 Surprised by Vegas Read More Katherine J. Reisfeld, CFP®, CIMA® 4/1/26 Katherine J. Reisfeld, CFP®, CIMA® 4/1/26 The Urge to Hedge: Why Chasing Reflation May Be the Riskiest Move You Make Read More Katherine J. Reisfeld, CFP®, CIMA® 3/23/26 Katherine J. Reisfeld, CFP®, CIMA® 3/23/26 Investing in Your Kid’s Future Read More Katherine J. Reisfeld, CFP®, CIMA® 3/18/26 Katherine J. Reisfeld, CFP®, CIMA® 3/18/26 Don't Miss April 15th: Your 2025 IRA Deadline and the Roth Strategies Worth Knowing Read More Katherine J. Reisfeld, CFP®, CIMA® 3/12/26 Katherine J. Reisfeld, CFP®, CIMA® 3/12/26 When You Can’t Get Your Money Back Read More Katherine J. Reisfeld, CFP®, CIMA® 3/12/26 Katherine J. Reisfeld, CFP®, CIMA® 3/12/26 What 35 Years of Data Taught Me About Investing Read More Katherine J. Reisfeld, CFP®, CIMA® 3/5/26 Katherine J. Reisfeld, CFP®, CIMA® 3/5/26 Stay Calm on the Markets — But Please Do This One Thing Read More Behavioral Coaching, Investing Scott Reisfeld 12/25/25 Behavioral Coaching, Investing Scott Reisfeld 12/25/25 Think Twice About Chasing The Biggest Stocks Read More Katherine J. Reisfeld, CFP®, CIMA® 12/8/25 Katherine J. Reisfeld, CFP®, CIMA® 12/8/25 Bitcoin and the Money Supply: What's the Real Story? Read More Katherine J. Reisfeld, CFP®, CIMA® 11/16/25 Katherine J. Reisfeld, CFP®, CIMA® 11/16/25 529 Plans: Building an Educational Legacy Read More Katherine J. Reisfeld, CFP®, CIMA® 5/15/25 Katherine J. Reisfeld, CFP®, CIMA® 5/15/25 Why Every Financial Plan Should Include a Power of Attorney Read More Katherine J. Reisfeld, CFP®, CIMA® 2/10/25 Katherine J. Reisfeld, CFP®, CIMA® 2/10/25 Navigating Tax Benefits: Life Insurance Loans vs. Surrendering Policies Read More Katherine J. Reisfeld, CFP®, CIMA® 1/24/25 Katherine J. Reisfeld, CFP®, CIMA® 1/24/25 The Psychology of Investing: How Behavioral Finance Shapes Financial Success Read More Wealth & Wellness, Financial Planning Katherine J. Reisfeld, CFP®, CIMA® 1/7/25 Wealth & Wellness, Financial Planning Katherine J. Reisfeld, CFP®, CIMA® 1/7/25 When Setting Goals, Use The Time To Reflect On What Is Most Important To You Read More Behavioral Coaching, Investing Katherine J. Reisfeld, CFP®, CIMA® 12/12/24 Behavioral Coaching, Investing Katherine J. Reisfeld, CFP®, CIMA® 12/12/24 Black Swans Read More Retirement Planning, Wealth & Wellness, Longevity Planning Katherine J. Reisfeld, CFP®, CIMA® 10/29/24 Retirement Planning, Wealth & Wellness, Longevity Planning Katherine J. Reisfeld, CFP®, CIMA® 10/29/24 Embracing Longevity: Planning for a Fulfilling Future Read More Investing Katherine J. Reisfeld, CFP®, CIMA® 10/2/24 Investing Katherine J. Reisfeld, CFP®, CIMA® 10/2/24 What Stock Investors and Roger Federer Have In Common Read More Older Posts

Katherine J. Reisfeld, CFP®, CIMA® 6/8/26 Katherine J. Reisfeld, CFP®, CIMA® 6/8/26 The Cost of Complexity Read More

Katherine J. Reisfeld, CFP®, CIMA® 5/26/26 Katherine J. Reisfeld, CFP®, CIMA® 5/26/26 Introducing Elena Spellman Read More

Katherine J. Reisfeld, CFP®, CIMA® 5/26/26 Katherine J. Reisfeld, CFP®, CIMA® 5/26/26 Is an AI Crash Coming? Read More

Katherine J. Reisfeld, CFP®, CIMA® 5/19/26 Katherine J. Reisfeld, CFP®, CIMA® 5/19/26 Surprised by Vegas Read More

Katherine J. Reisfeld, CFP®, CIMA® 4/1/26 Katherine J. Reisfeld, CFP®, CIMA® 4/1/26 The Urge to Hedge: Why Chasing Reflation May Be the Riskiest Move You Make Read More

Katherine J. Reisfeld, CFP®, CIMA® 3/23/26 Katherine J. Reisfeld, CFP®, CIMA® 3/23/26 Investing in Your Kid’s Future Read More

Katherine J. Reisfeld, CFP®, CIMA® 3/18/26 Katherine J. Reisfeld, CFP®, CIMA® 3/18/26 Don't Miss April 15th: Your 2025 IRA Deadline and the Roth Strategies Worth Knowing Read More

Katherine J. Reisfeld, CFP®, CIMA® 3/12/26 Katherine J. Reisfeld, CFP®, CIMA® 3/12/26 When You Can’t Get Your Money Back Read More

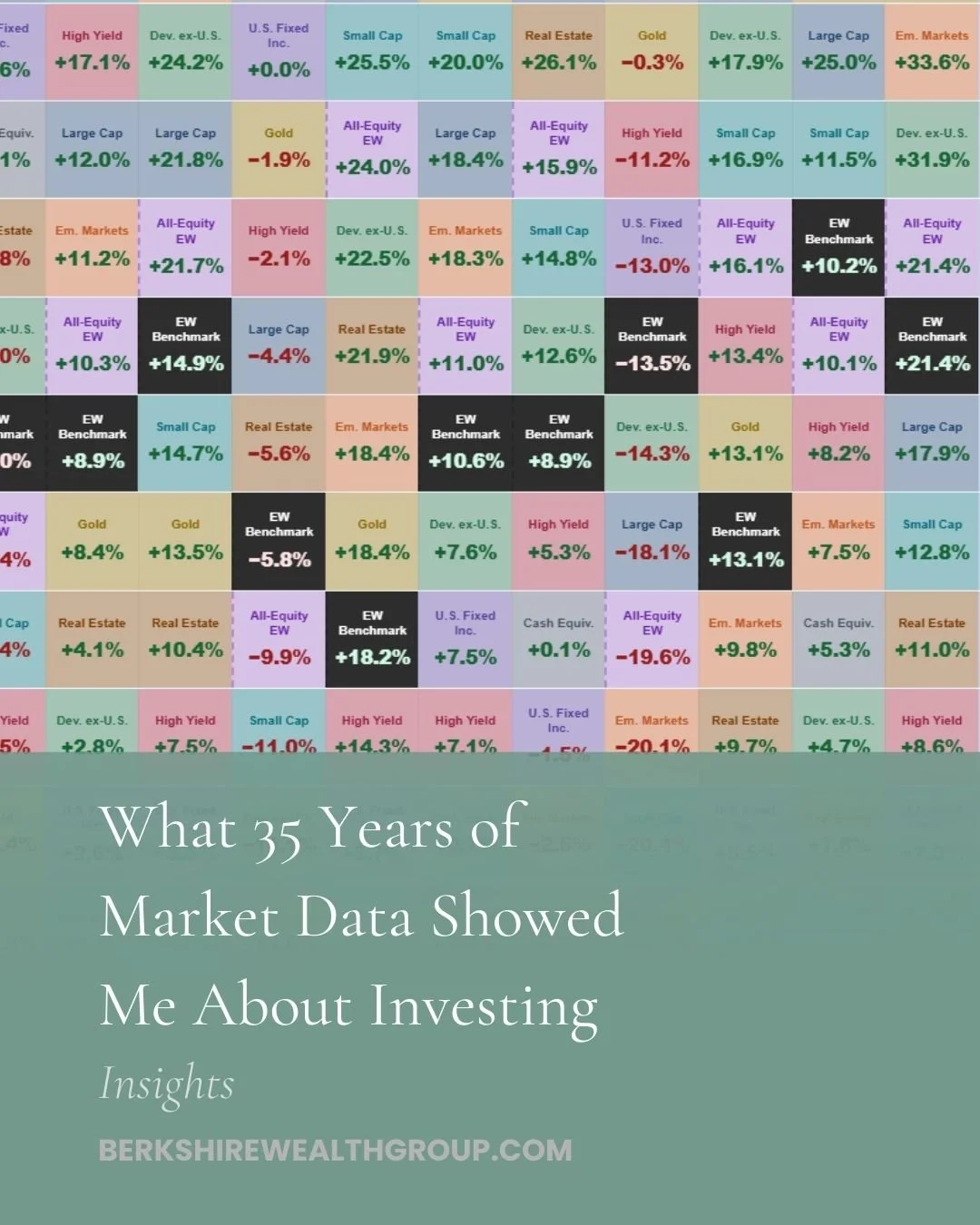

Katherine J. Reisfeld, CFP®, CIMA® 3/12/26 Katherine J. Reisfeld, CFP®, CIMA® 3/12/26 What 35 Years of Data Taught Me About Investing Read More

Katherine J. Reisfeld, CFP®, CIMA® 3/5/26 Katherine J. Reisfeld, CFP®, CIMA® 3/5/26 Stay Calm on the Markets — But Please Do This One Thing Read More

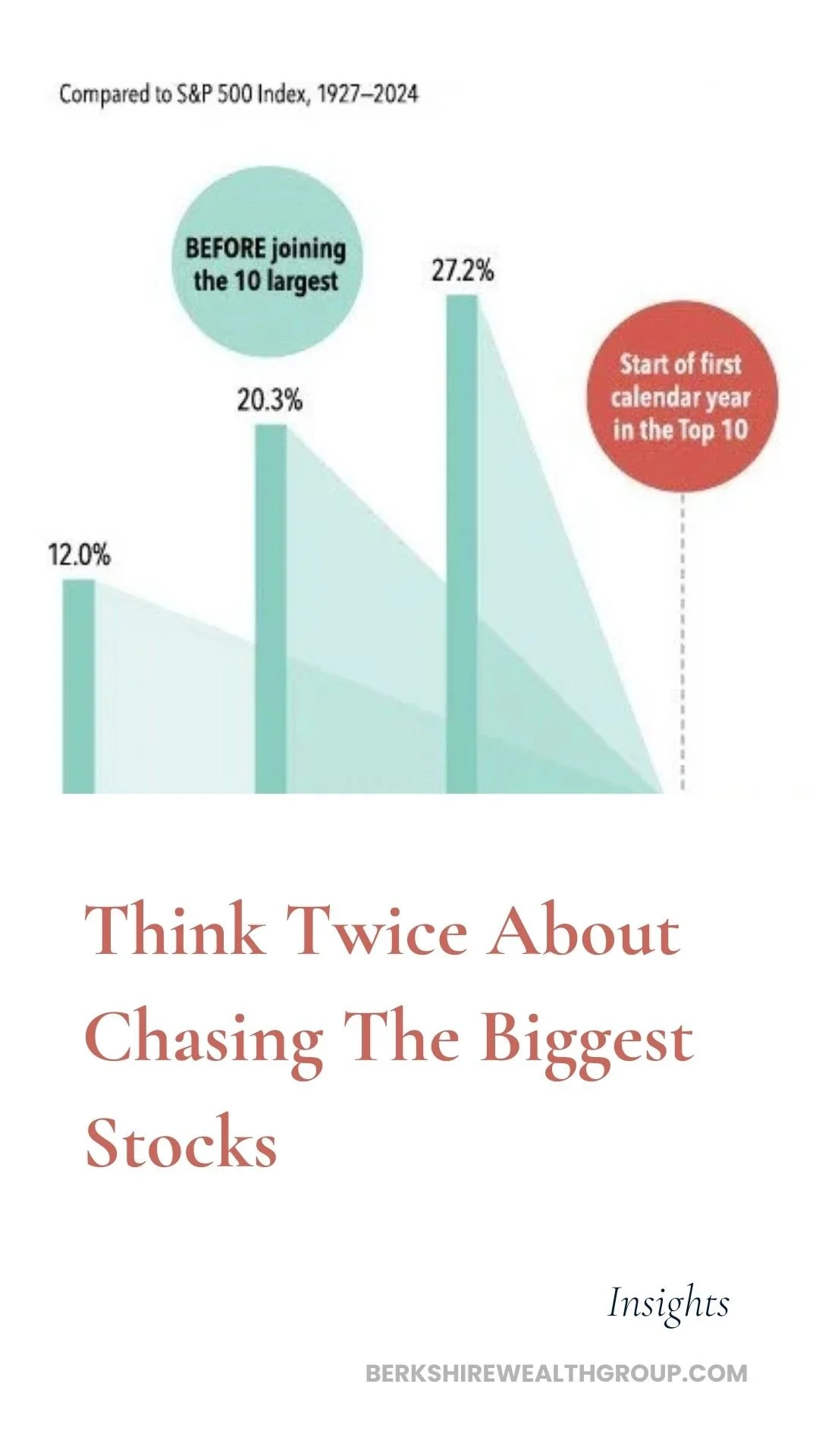

Behavioral Coaching, Investing Scott Reisfeld 12/25/25 Behavioral Coaching, Investing Scott Reisfeld 12/25/25 Think Twice About Chasing The Biggest Stocks Read More

Katherine J. Reisfeld, CFP®, CIMA® 12/8/25 Katherine J. Reisfeld, CFP®, CIMA® 12/8/25 Bitcoin and the Money Supply: What's the Real Story? Read More

Katherine J. Reisfeld, CFP®, CIMA® 11/16/25 Katherine J. Reisfeld, CFP®, CIMA® 11/16/25 529 Plans: Building an Educational Legacy Read More

Katherine J. Reisfeld, CFP®, CIMA® 5/15/25 Katherine J. Reisfeld, CFP®, CIMA® 5/15/25 Why Every Financial Plan Should Include a Power of Attorney Read More

Katherine J. Reisfeld, CFP®, CIMA® 2/10/25 Katherine J. Reisfeld, CFP®, CIMA® 2/10/25 Navigating Tax Benefits: Life Insurance Loans vs. Surrendering Policies Read More

Katherine J. Reisfeld, CFP®, CIMA® 1/24/25 Katherine J. Reisfeld, CFP®, CIMA® 1/24/25 The Psychology of Investing: How Behavioral Finance Shapes Financial Success Read More

Wealth & Wellness, Financial Planning Katherine J. Reisfeld, CFP®, CIMA® 1/7/25 Wealth & Wellness, Financial Planning Katherine J. Reisfeld, CFP®, CIMA® 1/7/25 When Setting Goals, Use The Time To Reflect On What Is Most Important To You Read More

Behavioral Coaching, Investing Katherine J. Reisfeld, CFP®, CIMA® 12/12/24 Behavioral Coaching, Investing Katherine J. Reisfeld, CFP®, CIMA® 12/12/24 Black Swans Read More

Retirement Planning, Wealth & Wellness, Longevity Planning Katherine J. Reisfeld, CFP®, CIMA® 10/29/24 Retirement Planning, Wealth & Wellness, Longevity Planning Katherine J. Reisfeld, CFP®, CIMA® 10/29/24 Embracing Longevity: Planning for a Fulfilling Future Read More

Investing Katherine J. Reisfeld, CFP®, CIMA® 10/2/24 Investing Katherine J. Reisfeld, CFP®, CIMA® 10/2/24 What Stock Investors and Roger Federer Have In Common Read More