Investing in Your Kid’s Future

Roth IRAs and the New Government-Backed Children’s Savings Accounts

One of the most meaningful gifts you can give a child isn’t wrapped in a box. It’s time — specifically, decades of tax-advantaged compounding that starts long before they ever enter the workforce. Two savings vehicles make this possible right now: the custodial Roth IRA, which has quietly been one of the best tools in family financial planning for years, and a brand-new government-backed children’s investment account established in 2025 that opens for contributions on July 4, 2026.

Used thoughtfully, they can be a powerful combination — but as with any savings tool, the details matter.

The Custodial Roth IRA: Starting the Clock Early

A custodial Roth IRA works just like a regular Roth IRA, with one key difference: a parent or guardian opens and manages it on behalf of a minor. When the child reaches adulthood — typically 18 or 21, depending on the state — the account becomes fully theirs.

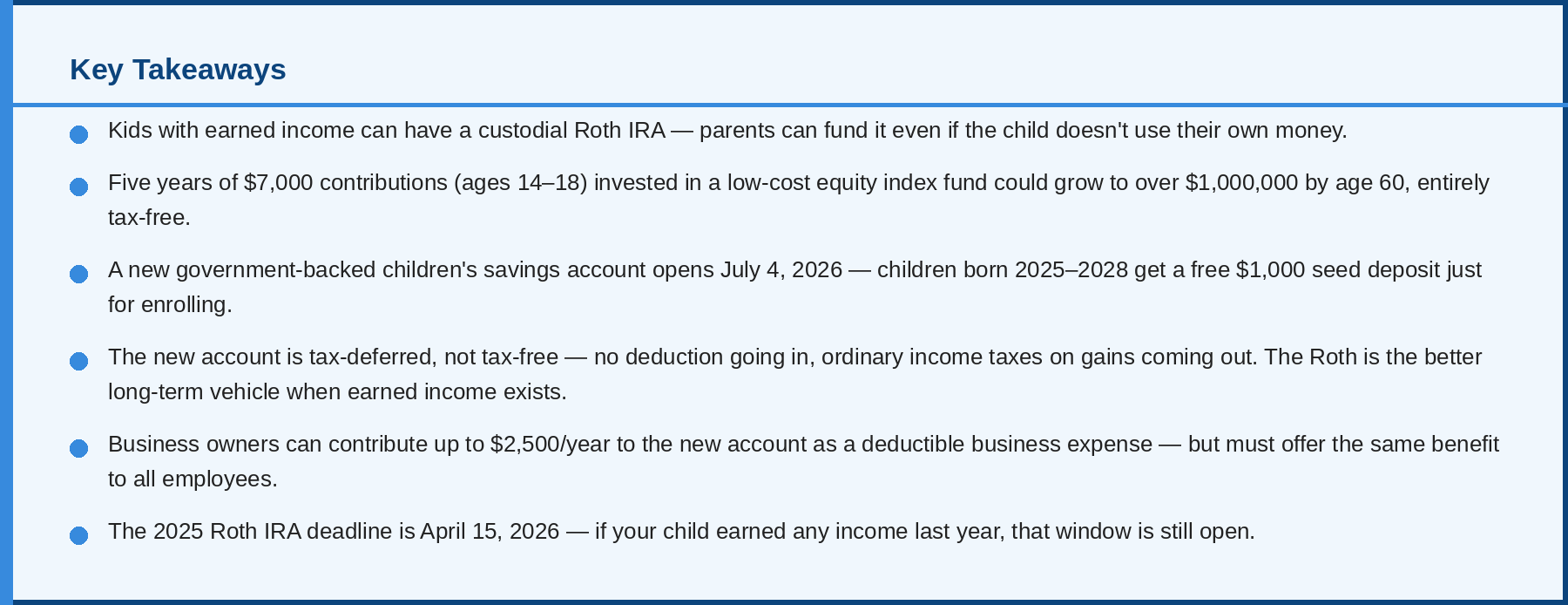

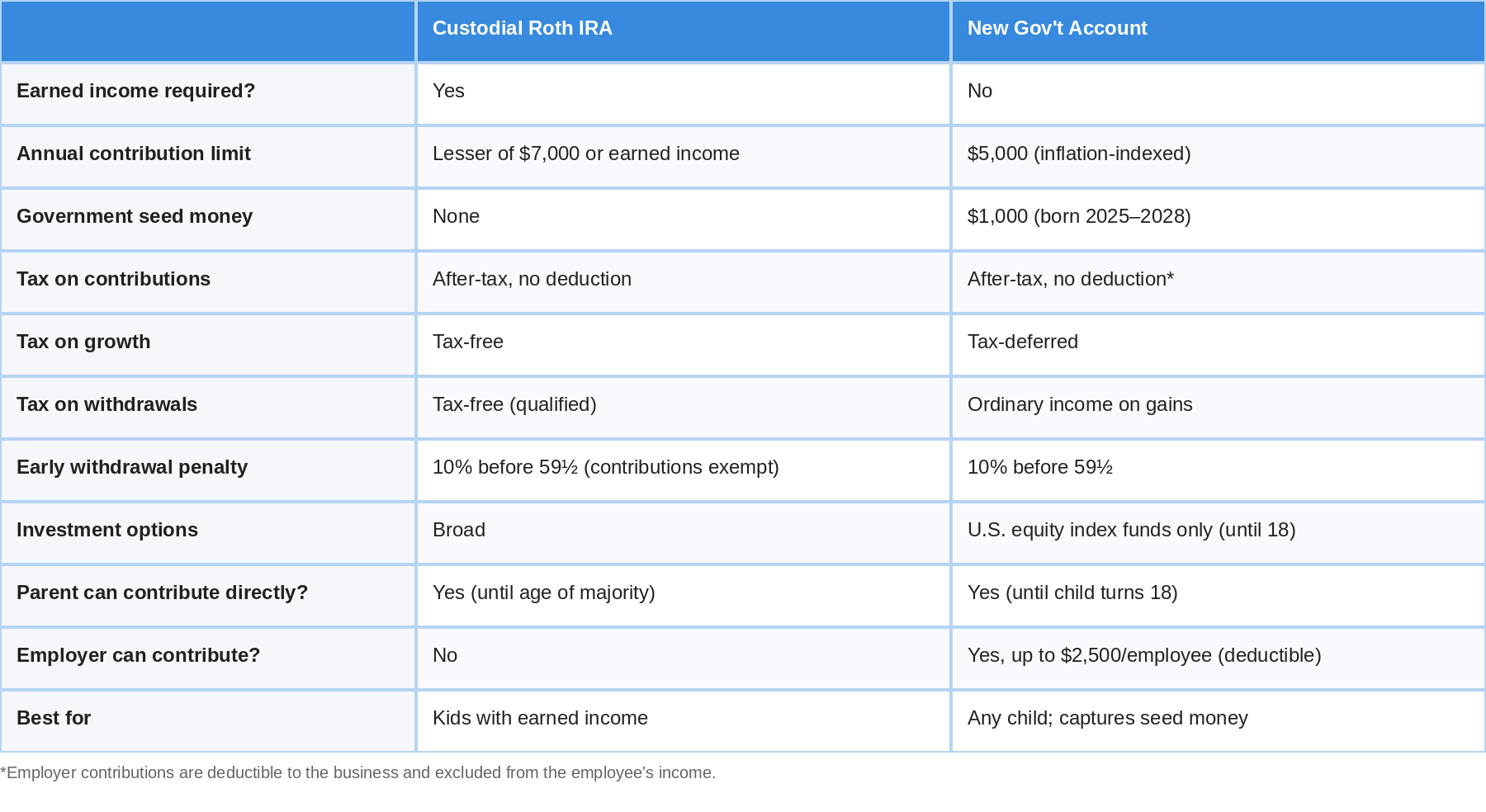

The most important rule to know upfront: the child must have earned income. You can’t contribute more than what the child actually earned that year, and you also can’t exceed the standard annual IRA contribution limit ($7,000 in 2025). So if your 14-year-old earns $2,500 babysitting or working a summer job, you can contribute up to $2,500 to their Roth IRA — even if the money comes from your own pocket. The child doesn’t have to use their own earnings; you simply can’t contribute more than what they made.

Why a Roth, and why start young?

The Roth’s biggest advantage is tax-free compounding. Contributions go in with after-tax dollars, but the growth is never taxed — and qualified withdrawals in retirement are completely tax-free too. For a child who’s likely in a very low tax bracket (or no bracket at all), the Roth is often a clear choice.

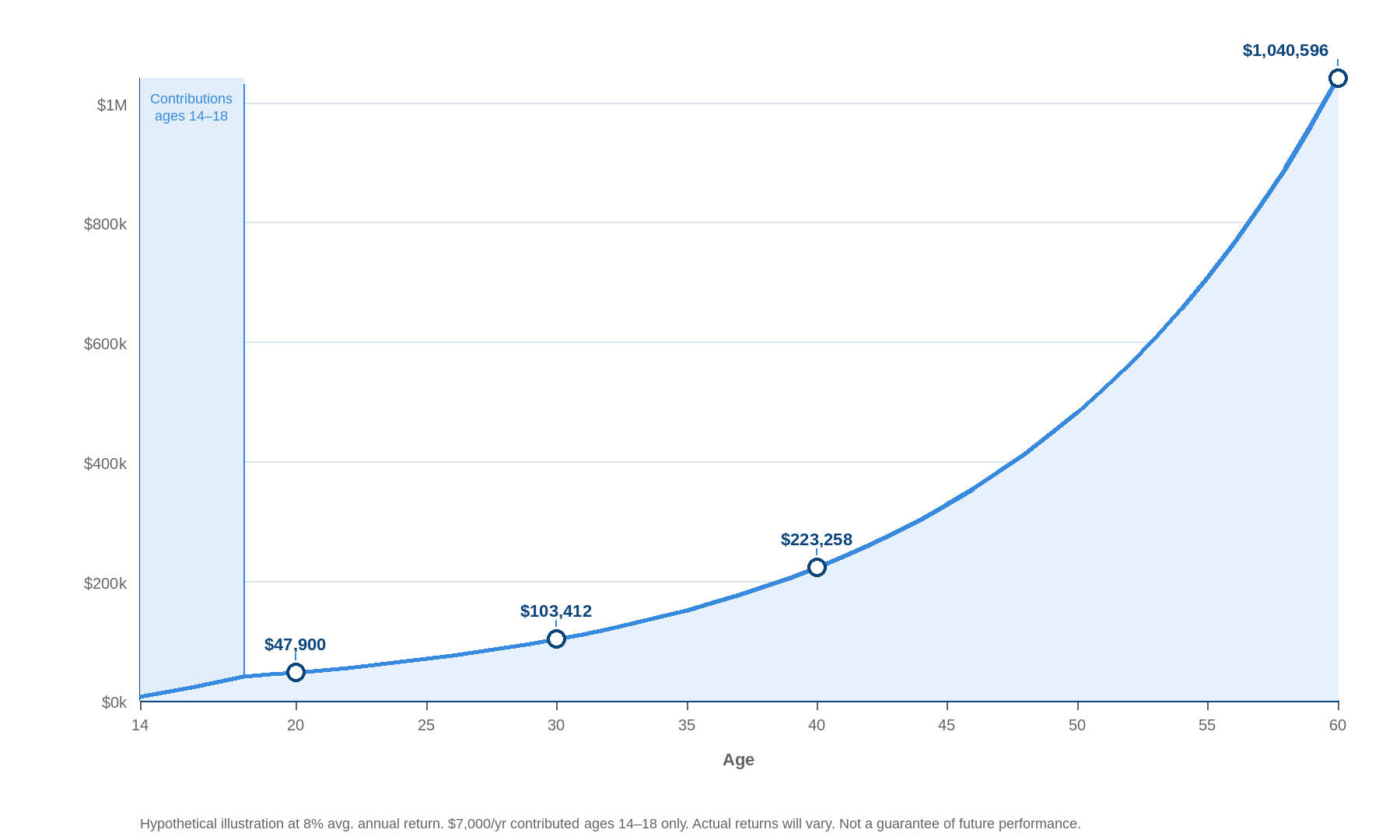

And when this money is invested entirely in a low-cost equity index fund — which is exactly where it belongs given a 40-plus year time horizon — the math becomes genuinely striking. A parent who contributes $7,000 per year from ages 14 through 18 — five years, $35,000 total — and never adds another dollar, would see that account grow to over $1,000,000 by the time the child reaches age 60, assuming an 8% average annual return. Every dollar of it tax-free.

There is simply no good reason to hold bonds or cash in an account with this kind of runway. Time is the risk management.

What counts as earned income?

Earned income includes wages from a W-2 job, net self-employment income (babysitting, lawn care, tutoring, or even social media content creation), and modeling or acting income. It does not include allowances, gifts, interest, or investment gains.

One important clarification worth stating plainly: regular household chores do not count. The IRS views tasks like washing dishes, making beds, taking out the trash, or doing laundry as normal family responsibilities — not employment. Contributions based solely on chore pay could be disqualified if ever scrutinized, so it’s worth being clear-eyed about this before making a contribution.

What does work is paying a child for tasks that go meaningfully beyond normal household duties — the kind of work you’d reasonably hire an outside person to do. For parents who own a business, this is where a genuine opportunity opens up. If your child helped out in your business in 2025 — filing, answering phones, running errands, helping with social media, or any other real task — that’s legitimate earned income. Document it, pay a reasonable wage, and it counts. The work needs to be real, the pay needs to be reasonable, and there needs to be a paper trail. The IRS is not interested in the dishes. It is, however, very interested in whether the work actually happened.

What happens when they turn 18?

Once your child reaches the age of majority in your state, the custodial account becomes fully theirs — they take over ownership and control, and the custodial structure ends. A parent can no longer contribute directly. That said, parents can absolutely continue supporting the account by gifting their child the funds to contribute themselves, provided the child has sufficient earned income and remains under the Roth income phase-out thresholds ($150,000 for single filers in 2025). The habit of annual contributions doesn’t have to stop at 18 — it just shifts from parent-controlled to a conversation worth having with your young adult.

It’s worth having that conversation thoughtfully before the transition happens, while the account is still under your management and the purpose of it is fresh.

The Power of Five Years: What $35,000 Can Become

Five years of maximum contributions — $7,000 per year from ages 14 through 18 — totals $35,000. Invested entirely in a low-cost equity index fund and left untouched, here is what that looks like at age 60 at an 8% average annual return:

$35,000 in. Over $1,000,000 out. Tax-free. The contributions stop at 18. The compounding doesn’t.

Hypothetical illustration at 8% average annual return. Contributions of $7,000/year made at ages 14–18 only. Actual returns will vary. Not a guarantee of future performance.

The New Government-Backed Children’s Investment Account: No Job Required

If your child doesn’t have earned income yet, or if you want to layer additional savings alongside a Roth IRA, a brand-new type of children’s investment account is becoming available in 2026.*

These accounts allow parents, guardians, and other individuals to contribute up to $5,000 per year for any child under age 18 — with no requirement that the child have earned income. The contribution limit is indexed to inflation over time.

The most compelling feature for families with young children: children born between January 1, 2025 and December 31, 2028 will receive a one-time $1,000 government-funded seed deposit to get the account started, with no income requirements to qualify. And for children who are too old to receive the federal seed money, Michael and Susan Dell have pledged $6.25 billion to provide $250 grants for up to 25 million children under age 10 who live in ZIP codes where the median household income is $150,000 or less.

So what’s the catch?

Here’s where parents need to read the fine print carefully — because this account is not as tax-advantaged as it might initially appear.

Contributions are not tax-deductible. Those contributing to these accounts do not receive a tax deduction, though contributions are not included in the income of beneficiaries. In other words, you put in after-tax dollars and get no deduction for doing so.

Earnings are not subject to tax until the money is distributed, but distributions are taxed as ordinary income on any gains above your original contributions. Think of it like a traditional IRA with a deduction you never got — you defer taxes on the growth, and then pay them at ordinary income rates when the money comes out.

Additionally, because the accounts follow standard IRA distribution rules, a 10% early withdrawal penalty applies to funds taken out before age 59½, with limited exceptions for qualifying education expenses and first-time home purchases.

What can the money be invested in?

Contributions must be invested in a mutual fund or ETF with annual fees of no more than 0.1% that tracks a qualified index of U.S. equities — think S&P 500 index funds. No bonds, no international holdings, no individual stocks during the child’s minor years. Investment options broaden to standard IRA rules after the child turns 18.

Who can open one?

The child must be a U.S. citizen, and at least one parent must have a valid Social Security number. The accounts open for contributions on July 4, 2026. Parents can start the enrollment process now by filing Form 4547 with their 2025 federal income taxes, or through an online portal expected to launch around the same time.

A Closer Look: Is the Tax Treatment Really Worth It?

This is a fair and important question — and worth sitting with.

The new government-backed account offers tax-deferred growth but no tax deduction on contributions and no tax-free treatment on withdrawals. You’re deferring taxes, not eliminating them. That’s a meaningful distinction compared to a Roth IRA, where both the growth and the qualified withdrawals are completely tax-free.

So what about simply investing in a regular, well-managed taxable account for your child?

For long-term, buy-and-hold investing using tax-efficient funds — broad index funds with low turnover — a taxable account can actually behave quite favorably. Unrealized gains aren’t taxed until you sell. Qualified dividends and long-term capital gains are taxed at preferential rates, potentially 0% for lower-income individuals. And unlike the new government account, there are no restrictions on investments, no penalties for early access, and no mandatory wait until age 59½.

The honest comparison: the new account wins most clearly in two scenarios — when the $1,000 (or $250) seed money is in play, or when an employer is contributing on the child’s behalf tax-free. Those are genuinely valuable, and the seed money alone is worth capturing. But if you’re funding the account entirely on your own with after-tax dollars, no deduction, and ordinary income taxes owed on gains at withdrawal, a Roth IRA (when the child has earned income) or a thoughtfully managed taxable account may well serve your child better in the long run.

The bottom line: for families with newborns born between 2025 and 2028, opening the account to capture the $1,000 seed money is almost certainly worth doing — that’s free money with decades to grow. Beyond that, how much additional you contribute each year deserves a more nuanced conversation.

A note for business-owning families

This is where the new account starts to look meaningfully more interesting. An employer can establish a Section 128(c) Trump account contribution plan for employees or their dependents, and employer contributions are a deductible business expense. The limit is $2,500 per year per employee — not per child.

How the employer contribution works

As a business owner, you can contribute up to $2,500 per year to your child’s account as a deductible business expense — provided you establish a formal Trump Account Contribution Program (TACP) and offer the same benefit to all of your employees.

If both spouses are employees of the business, each may have a separate $2,500 entitlement, potentially covering the full $5,000 annual limit with pre-tax business dollars — though this specific scenario isn’t yet explicitly addressed in IRS guidance and is worth confirming with your CPA once the Section 128 regulations are finalized.

One practical note: if your other employees have no children under 18, there is no benefit for them to receive — which largely neutralizes the nondiscrimination concern for small practices with limited eligible dependents. But the plan must genuinely be available to all employees, not just the owners.

This is not a DIY decision — but it’s one worth putting on the agenda with your accountant once the Section 128 guidance drops later in 2026.

How the Accounts Compare at a Glance

*Employer contributions to the new government-backed account are deductible to the business and excluded from the employee’s income. Individual contributions are after-tax with no deduction.

Both accounts can be held simultaneously, and neither affects the other’s contribution limits.

Don’t Miss the 2025 Roth IRA Deadline for Your Teen

If your child turned 14 at any point in 2025 and had any earned income, you have until April 15, 2026 to make a 2025 Roth IRA contribution on their behalf.

This is one of those rare moments where the calendar works in your favor. You can fund the 2025 contribution today, right now, even though the year has already ended. The IRS allows prior-year contributions until Tax Day.

The contribution limit is $7,000, or the child’s total 2025 earned income — whichever is lower. You don’t have to use the child’s actual dollars; parents can fund it directly. What matters is that the income existed.

Every year you miss this window is a year of tax-free compounding you can’t get back. A 14-year-old who starts today has over 45 years of runway before traditional retirement age. That’s not a small thing.

What to do before April 15

1. Add up your child’s 2025 earned income — W-2 wages, self-employment, babysitting, coaching, family business work, or any other real work income.

2. Open a custodial Roth IRA if one isn’t already in place.

3. Contribute up to the lesser of $7,000 or the child’s total 2025 earned income, and designate it as a 2025 contribution before April 15.

4. Invest in a broadly diversified, low-cost equity index fund — and let the clock run.

A note for parents who own a business

If your child helped out in your business in 2025 — answering phones, filing, running errands, helping with social media, or any other real task you’d otherwise pay someone to do — that’s legitimate earned income. Document it, pay a reasonable wage, and it counts. We’re not suggesting anything about the dishes, of course. The IRS isn’t interested in the dishes.

The Biggest Variable Is Time

No matter which account you choose, the most powerful ingredient is the same: starting early. A dollar invested for a child at birth has roughly six times the compounding runway of a dollar invested when that same child turns 25. The specific vehicle matters far less than the habit of consistent, early investing.

The new government-backed accounts are still being finalized — additional IRS and Treasury guidance is expected before the July 2026 launch. If you’re thinking about the next generation’s financial foundation, now is a good time to revisit these options and think about what combination makes the most sense for your family.

* These accounts are established under Section 530A of the Internal Revenue Code and are commonly referred to as Trump Accounts or 530A accounts.

This article is for informational and educational purposes only and does not constitute personalized financial, tax, or legal advice. Please consult your tax advisor regarding your specific situation before making any contribution decisions.