Don't Miss April 15th: Your 2025 IRA Deadline and the Roth Strategies Worth Knowing

⏰ ACTION REQUIRED — 2025 IRA Contribution Deadline: April 15, 2026

You still have time to make a 2025 IRA contribution — but the window closes April 15th. This applies to all three types:

• Traditional (deductible) IRA: Contribute pre-tax and potentially deduct it on your 2025 return.

• Roth IRA (direct): If your income is below the phase-out threshold, contribute after-tax for tax-free growth.

• Non-deductible (after-tax) IRA: The first step of the Backdoor Roth strategy described below — available regardless of income, and eligible for immediate conversion to Roth.

The 2025 limit is $7,000 per person, or $8,000 if you were age 50 or older as of December 31, 2025. Not sure which type applies to you? Reach out — we’re happy to help you figure it out before the deadline.

The Backdoor Roth and the Mega Backdoor Roth — and why higher earners should know about both.

If you've ever been told you make "too much" to contribute to a Roth IRA, you're not alone — and it's not the end of the story.

Roth accounts are one of the most powerful tools in retirement planning. Money goes in after you've paid taxes on it, grows completely tax-free, and comes out in retirement with no taxes owed. The IRS does limit who can contribute directly to a Roth IRA based on income — but there are two well-established, fully legal workarounds that allow higher earners to capture the same benefits.

They're called the Backdoor Roth IRA and the Mega Backdoor Roth. Here's a plain-language guide to both.

Why Roth Matters

Most retirement accounts fall into one of two tax buckets. Traditional accounts (pre-tax 401(k)s, deductible IRAs) give you a tax break now — but you'll pay income taxes on every dollar you withdraw in retirement. Roth accounts flip the equation: you pay taxes now, and withdrawals in retirement are completely tax-free.

For people who expect to be in a higher tax bracket later — or who simply want flexibility and tax-free income in retirement — Roth accounts are exceptionally valuable. The problem is the income ceiling. In 2025, the ability to contribute directly to a Roth IRA phases out between $150,000 and $165,000 for single filers, and between $236,000 and $246,000 for married couples filing jointly. Earn above those thresholds, and the direct route is closed.

But the conversion route is always open. That's the key.

The Backdoor Roth IRA

The Backdoor Roth is a two-step process. It works because while there are income limits on contributing directly to a Roth IRA, there are no income limits on converting a traditional IRA to a Roth IRA.

Step 1: Make a non-deductible traditional IRA contribution.

Contribute up to $7,000 (or $8,000 if you're 50+) to a traditional IRA. Because your income is too high to deduct the contribution, it goes in on an after-tax basis. This is called a non-deductible contribution. Remember: you have until April 15th to do this for tax year 2025.

Step 2: Convert the traditional IRA to a Roth IRA.

Shortly after making the contribution, convert the traditional IRA to a Roth. Because you already paid taxes on the money, you owe little to no additional tax on the conversion — especially if you act quickly before any investment gains accumulate.

Step 3: File IRS Form 8606.

This form tracks your after-tax basis in the IRA, which is critical to avoid being taxed twice on money you've already paid taxes on. Don't skip it.

The One Catch: The Pro-Rata Rule

The Backdoor Roth works cleanly only if you don't have pre-tax money sitting in other traditional, SEP, or SIMPLE IRAs. If you do, the IRS requires you to calculate taxes proportionally across all your IRA assets — not just the new non-deductible contribution.

A simple example:

• You have $90,000 in a pre-tax rollover IRA and contribute $10,000 non-deductibly.

• Your total IRA balance is now $100,000. Only 10% is after-tax.

• When you convert $10,000 to Roth, only $1,000 of it is tax-free. The other $9,000 is taxable.

If you have pre-tax IRA balances, there are strategies to address this — including rolling those funds into a workplace 401(k) to clear the deck. It's worth a conversation before you act.

The Mega Backdoor Roth

If the Backdoor Roth IRA lets you sneak $7,000 a year into tax-free territory, the Mega Backdoor Roth opens a much larger door — potentially $20,000 to $40,000 more per year, depending on your plan. It lives inside your 401(k), not your IRA, and it works by exploiting the gap between the standard employee contribution limit and the IRS's much higher overall plan limit.

One important note: unlike IRA contributions, which can be made up until April 15th for the prior year, Mega Backdoor Roth contributions run through your 401(k) payroll and cannot be made retroactively. If this strategy is new to you, the time to set it up is now — for 2026.

Understanding the Gap

Most people know you can contribute up to $23,500 to a 401(k) in 2025 ($31,000 if you're 50+). What fewer people know is that the IRS allows a much higher total contribution to a 401(k) when you count all sources — your contributions, your employer's match, and after-tax employee contributions. That overall limit is $70,000 in 2025 ($77,500 if 50+).

The Mega Backdoor Roth uses that gap — the space between what you've already contributed and the $70,000 ceiling — to funnel additional after-tax dollars into a Roth account.

Step 1: Max out your regular 401(k) contributions.

Contribute your full employee deferral limit first — $23,500 (or $31,000 if 50+).

Step 2: Make after-tax contributions to your 401(k).

If your plan allows it, contribute additional after-tax (non-Roth) dollars up to the overall $70,000 limit, minus what you and your employer have already put in. For many people, this gap is $20,000 or more.

Step 3: Convert to Roth.

Move those after-tax dollars into a Roth account — either through an in-plan Roth conversion (if your plan allows it) or by rolling them out to a Roth IRA when you separate from service. Because the contributions were already after-tax, you owe little to no additional tax.

The Important Catch: Your Plan Has to Allow It

The Mega Backdoor Roth isn't available in every 401(k). Your plan must specifically allow after-tax employee contributions, and either in-plan Roth conversions or in-service withdrawals. Many large company plans include these features — but many don't. If you're unsure, the plan document or a quick call to your HR department will tell you. We're also happy to help you read through the details.

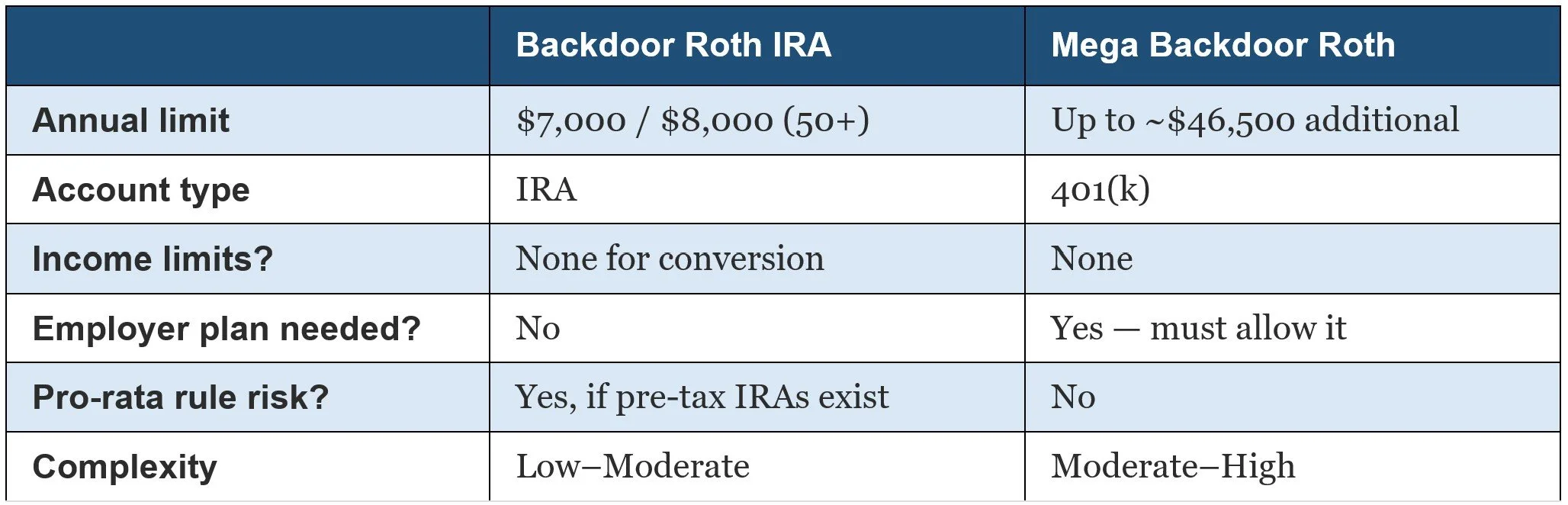

At a Glance: How They Compare

Is One of These Right for You?

These strategies work best for high earners who want to build tax-free retirement income, expect their tax rate to be higher in the future, or simply want more flexibility in how they draw down assets down the road. They're not for everyone — your existing IRA balances, your employer's plan, and your overall financial picture all play a role.

And if you've been sitting on the fence about your 2025 IRA contribution: the deadline is April 15th. That's soon. If a Backdoor Roth makes sense for your situation, now is the time to act.

We're happy to walk through either strategy with you in detail — whether you're deciding between them, need help checking your plan documents, or just want to make sure you're not leaving tax-free growth on the table. But please don’t leave it off till the last minute.

This post is for educational purposes only and does not constitute tax or legal advice. Contribution limits reflect 2025 IRS guidelines. Contributions to a traditional IRA may be tax-deductible depending on the taxpayer's income, tax-filing status, and other factors. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty. Earnings withdrawn prior to 59 1/2 would be subject to income taxes. Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Like Traditional IRAs, contribution limits apply to Roth IRAs. In addition, with a Roth IRA, your allowable contribution may be reduced or eliminated if your annual income exceeds certain limits. Contributions to a Roth IRA are never tax deductible, but if certain conditions are met, distributions will be completely income tax free. Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Additionally, each converted amount may be subject to its own five-year holding period. Converting a traditional IRA into a Roth IRA has tax implications. Investors should consult a tax advisor before deciding to do a conversion. IRA tax deductibility and contribution eligibility may be restricted if your income exceeds certain limits, please consult with a financial professional for more information.